Introduction

Latin America has firmly positioned itself as an emerging market for biodiesel, witnessing significant growth within its biofuel sector, which plays a pivotal role in the region’s energy landscape. Biodiesel has emerged as a prominent renewable fuel option.

Brazil, Argentina, and Colombia lead the production of biofuels in Latin America, boasting well-established industries in this sector. Latin American biodiesel is produced from diverse feedstocks, including soybean oil, palm oil, and used cooking oil.

Brazil stands out as a major biodiesel producer in Latin America, with a firmly established industry, focusing on soybean oil as the primary feedstock. Notably, Brazil predominantly consumes its biodiesel production domestically, unlike Colombia and Argentina.

Argentina emerges as another significant player in the biodiesel market, boasting a substantial export market. Soybean oil serves as the primary feedstock for biodiesel production in Argentina.

Colombia has also carved a niche in biodiesel production, primarily sourced from palm oil, with a notable presence in the export market.

In 2016, hydropower held the reins as the primary renewable energy source in Latin America, with biofuel contributing approximately 9% of the total energy mix. However, over the years, biodiesel has steadily gained a larger market share within the Latin American energy landscape.

Brazil

Brazil ranks as the third-largest producer and consumer of biodiesel globally, following Indonesia and the United States. According to a report by the United States Department of Agriculture (USDA), Brazilian biodiesel production surged to 7.1 billion litres in 2023, marking a 5 percent increase from the previous year’s volume of 6.7 billion litres. Biodiesel consumption reached 7.15 billion litres in 2023, up by 6 percent from the previous year.

In December 2023, the Brazilian government announced a significant policy shift by increasing the mandatory biodiesel admixture from 12 to 14% blend (B14), effective from March 2024 onwards. Additionally, there were indications of a potential further increase in the blending rate to reach 15% (B15) by 2025.

According to the Brazilian National Agency for Petroleum, Natural Gas and Biofuels (ANP), Brazil currently boasts 59 authorised biodiesel plants, with almost 60 percent of these plants are situated in the Centre-West region, benefitting from abundant soyabean supply.

Soybean oil dominates Brazil’s biodiesel industry, accounting for 69 percent of production, followed by greasy material at 16.2 percent, animal fat at 7.9 percent and palm oil at 2.4 percent. The industry’s utilization of tallow as a biodiesel feedstock has continued to decline, influenced by growing exports of tallow from Brazil to the U.S. The shift to higher biodiesel blends could reduce soybean oil exports, with each percentage point increase in the blend requiring an additional demand of 400,000 tonnes per year.

Table 1: Use of feedstock for biodiesel in Brazil (estimation, in ‘000 tonnes) (Oil World, 2023).

|

|

Jan/Dec 2023 |

Jan/Dec 2022 |

|

Soybean oil |

4,558 |

3,559 |

|

Tallow |

385 |

435 |

|

Palm oil |

163 |

117 |

|

Cotton oil |

98 |

68 |

|

Others |

1,383 |

1,294 |

Despite increased domestic consumption, Brazil exported 2.4 million tonnes of soybean oil in 2023, a 7.8 percent decrease from 2022. This trend may continue in 2024 due to the growing use of soybean oil in biodiesel production.

Argentina

Argentina emerges as another potential biodiesel producer in the region, with its biodiesel production primarily reliant on soybean oil. The country has successfully developed an export market for its biodiesel.

The Argentine biodiesel industry comprises two distinct sectors: small and medium-sized plants catering to the domestic market under the biodiesel mandate, and large plants, focused on exporting their production. Regardless of size, biodiesel plants in Argentina predominantly utilises soybean oil as their feedstock.

However, Argentina grapples with persistent political and financial uncertainty, marked by ongoing currency devaluation and high inflation rates, which significantly impact the growth of its biodiesel industry.

Biodiesel production in Argentina plummeted to an almost record low level of 1 billion litres in 2023, attributed to weak diesel demand, low blending ratios, and reduced exports. Biodiesel exports were sluggish in the first half of 2023 due to uncompetitive pricing in the European Union (EU), with a forecast of 280 million litres for 2023. Domestic biodiesel demand is expected to decrease due to reduced diesel demand and lower mandated blending rates.

Soybean oil consumption for biodiesel is anticipated to remain minimal in the first quarter of 2024, depending onpotential government policy changes. Argentina is poised to export a larger share of its soybean oil production, with an increase in exports to the U.S. biodiesel industry.

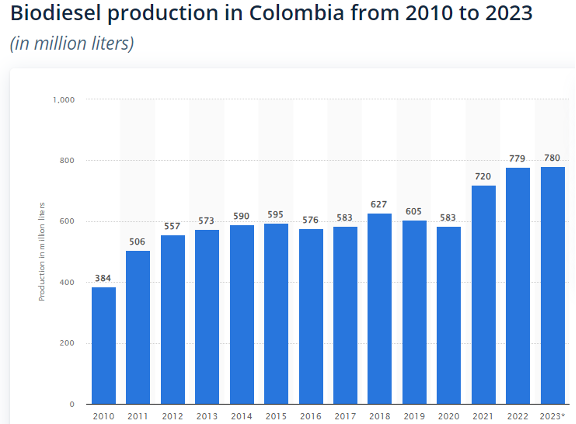

Colombia

Colombia has made significant strides in biodiesel production, primarily utilizing palm oil as its main feedstock. The country benefits from abundant year-round palm oil production, facilitated by its tropical climate and conducive environmental conditions for oil palm cultivation. Organisations like the National Federation of Palm Oil Farmers (Fedepalma), actively support biofuel production by assisting oil palm farmers.

The fuel market in Colombia is tightly regulated by the Ministry of Mines and Energy (MME), which sets biofuel blending mandates, regulates fuel and biofuel prices, and establishes technical regulations on biofuel standards. The biodiesel blending mandate currently stands at B10.

According to the United States Department of Agriculture (USDA), Colombia’s biodiesel production was forecasted to reach 780 million litres in 2023, bolstered by robust domestic production and a stable blending mandate. In 2022, biodiesel production in the country amounted to 779 million litres, marking an 8.2 percent increase from the previous year. Colombia is home to 12 operational biodiesel plants, all utilising palm oil as feedstock.

An estimated 687,000 tonnes of palm oil were consumed for biodiesel production in Colombia in 2023, with used cooking oil being utilised on a smaller scale, amounting to approximately 35,000 tonnes.

Figure 1: Biodiesel production in Colombia from 2012 to 2023 (Statista, 2024).

Colombia’s economic growth slowed in 2023, exacerbated by rising gasoline prices due to the gradual removal of government subsidies. This trend is expected to impede significant growth in fuel consumption, including biodiesel, moving forward.

United States

The United States has seen a notable rise in renewable fuel production, including biodiesel, driven by the U.S. Renewable Fuel Standard (RFS), which mandates blending renewable fuel into traditional fossil fuels.

Biodiesel consumption and production in the U.S have grown substantially since the early 2000s, largely attributed to various state and federal government incentive programmes. In 2023, renewable diesel and other biofuels production in the U.S. reached 3 billion gallons, expected to increase to 7.4 billion gallons after 2025. The country is rapidly constructing renewable diesel plants, including the Phillips 66 plant in Rodeo, California, one of the world’s largest renewable refineries, boasting a production capacity of 680 million gallons.

This growth has led to increased usage of U.S. soybean oil in biofuel production, with nearly 45 percent of biodiesel feedstocks derived from soybean oil. Consequently, the U.S. became a net importer of soybean oil in 2023-24, marking a significant shift from its historical role as a leading exporter.

Table 2: United States usage of feedstock for biodiesel and HVO (in ‘000 tonnes) (EIA, 2024).

|

|

Jan/Dec 2023 |

Jan/Dec 2022 |

|

Soybean oil |

5,906 |

4,774 |

|

Corn oil |

1,753 |

1,584 |

|

Canola oil |

1,534 |

640 |

|

Tallow/Grease |

2,331 |

1,346 |

|

Used oil |

3,432 |

2,633 |

|

Total |

14,956 |

10,977 |

In 2023, U.S. consumption of soybean oil rose by 8 percent to 12.25 million tonnes, primarily driven by usage in biofuels, while production reached 12.03 million tonnes. However, increased demand for soybean oil has led to a surge in imports of other oils and fats, including rapeseed oil, palm oil, and tallow/grease.

Table 3: United States soybean oil balance (in ‘000 tonnes) (Oil World, Dec 2023).

|

|

2023 |

2022 |

2021 |

|

Production |

12,032 |

11,785 |

11,434 |

|

Consumption |

12,257 |

11,348 |

10,701 |

|

Imports |

190 |

127 |

153 |

|

Exports |

161 |

637 |

724 |

Table 4: Increasing U.S. imports of rapeseed oil, palm oil, and tallow / grease in 2021-2023 (in ‘000 tonnes) (Oil World, Dec 2023).

|

|

2023 |

2022 |

2021 |

|

Rapeseed oil |

2,980 |

2,140 |

1,969 |

|

Palm oil |

1,816 |

1,713 |

1,693 |

|

Tallow/Grease |

760 |

597 |

362 |

U.S. imports of oils and fats surged to 7.39 million tonnes in 2023, a 15 percent increase from the previous year. Reduced exports from the U.S, Argentina, and Brazil may have a profound impact on the global oils and fats trade.

*Disclaimer: This document has been prepared based on information from sources believed to be reliable but we do not make any representations as to its accuracy. This document is for information only and opinion expressed may be subject to change without notice and we will not accept any responsibility and shall not be held responsible for any loss or damage arising from or in respect of any use or misuse or reliance on the contents. We reserve our right to delete or edit any information on this site at any time at our absolute discretion without giving any prior notice.